Introduction

HB73 (Act 2024-344) and the accompanying administrative rule 810-4-1-.28, introduces a cap mechanism that limits the annual increase in the taxable assessed value of Class II and Class III real properties. Property taxes are an essential source of funding for community services, including schools, public safety, and infrastructure. Understanding how property values are assessed and taxed helps taxpayers navigate changes and ensures transparency in the process.

The base year for implementing this change was effective October 1, 2024, for tax collections beginning October 1, 2025. New rules will cap annual increases in taxable assessed value for Class II and Class III real properties at 7 percent.

Use the sections below to explore key features of this new legislation, understand its application, and learn how it may affect your property taxes.

General Information

What Is the Cap?

The cap limits the annual increase in taxable assessed values of Class II (e.g., commercial properties) and Class III (e.g., agricultural or owner-occupied residential properties) to 7 percent. This cap ensures that property taxes increase gradually, even during periods of rapid market appreciation.

When Does the Cap Apply?

The cap applies to properties already assessed under the Class II or Class III classifications. Properties are evaluated annually, and the cap is applied when the property’s true assessed value increases by more than 7 percent compared to the prior year’s taxable assessed value.

Are there exceptions to the Cap?

Certain events trigger the removal of the cap, meaning the property will be reassessed based on its full, true assessed value. These include:

- The property is located in a tax increment district pursuant to Chapter 99 of Title 11, Code of Ala. 1975.

- The property’s assessment classification pursuant to §40-8-1, Code of Ala. 1975 changed. For example, reclassifying a property from residential (Class 3), to commercial (Class 2).

- The property changed ownership. This condition would not be met if the change in ownership is between spouses or family members for no or nominal consideration or because of the original owner’s death. This condition would not be met if the change in ownership is due to redemption after foreclosure of a mortgage, tax sale, or tax lien.

- Class II or Class III real property that has never been assessed. This would include escapes, pursuant to §40-7-23, Code of Ala. 1975, and a newly added improvement of any type to the parcel, such as a single-family home, canopy, or swimming pool that has never been assessed.

- An addition has been added to the parcel, or a significant improvement has been made to the property. Ordinary maintenance to existing improvements on the parcel or its grounds do not meet this condition.

How Is the Cap Calculated?

- If the cap applies, the current taxable assessed value is set to 1.07 times the prior year’s taxable assessed value, rounded to the nearest $20 increment that does not exceed the 7 percent cap.

- If the property’s true assessed value falls below the capped value during a market downturn, the taxable value aligns with the true assessed value.

What this Means for You

- Tax Predictability: Gradual changes in taxable assessed value help property owners plan for their tax bills.

- Protection Against Volatility: The cap mitigates the effects of sharp market fluctuations, preventing sudden spikes in taxes during periods of rapid market growth. Your taxable value will not spike dramatically, even if market values in your area increase significantly.

- During Market Downturns: The cap smooths the effects of market declines, ensuring a more stable tax base for local governments and consistent property tax bills for you.

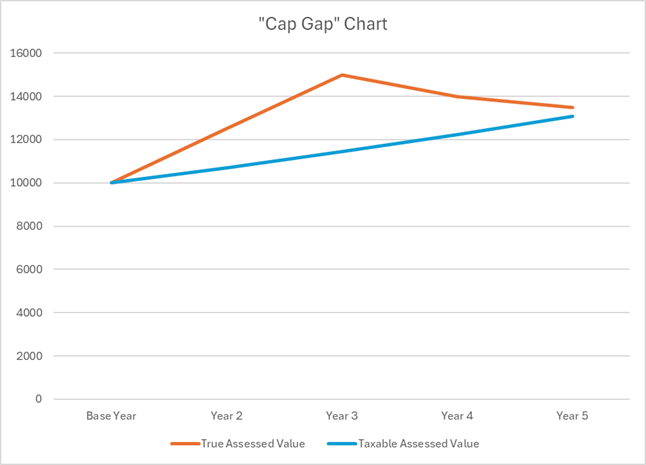

How the Cap Works During Market Downturns – Understanding the Cap Gap

The cap mechanism not only limits increases in taxable assessed values during market growth but also affects how taxable values adjust during market downturns. A key aspect of this is the “cap gap.”

What Is the Cap Gap?

In years when market values increase rapidly, the cap limits the increase in taxable (capped) assessed values to +7%. This creates a “gap” between the true assessed value, (which is tied directly to market or use value) and the taxable (capped) assessed value. During a market downturn, the taxable assessed value will continue to rise (according to the cap), until the taxable assessed value becomes the lessor of the preceding year taxable (capped) assessed value x 1.07 OR the current true assessed value. The lagging effect means that just as taxable “capped” assessed values lag in times of hyperinflation, the capped values will also lag in times of market downturns.

The Cap Gap in Market Downturns

Because of the “gap” created between true assessed value and taxable (capped) assessed value, you may still see increases in taxable assessed values, even during times of market downturns. For example, in the illustration presented below, between years 3,4, and 5, the true assessed value (top line) decreased. Because of the lagging effect, the capped taxable value will still increase until True Assessed and Taxable Assessed are equalized.

How Does This Affect You?

- Continued Taxable Value Growth: Even as market values decline, your taxable value may continue to rise, creating a delay in reflecting the lower market conditions.

- Alignment with Market Value: If the market downturn is prolonged, eventually, the true assessed value might fall below the capped assessed value, at which point the capped assessed value would stabilize and align with the true assessed value.

- Smoothing Effect: This gradual adjustment prevents abrupt decreases in taxable values, which helps local governments maintain stable revenue streams for public services, even during economic downturns.

Frequently Asked Questions (FAQs):

I am purchasing a property. Can I rely on the current owner’s taxes as a good indication of future tax liabilities?

No. When buying real estate, do not assume the property taxes will remain the same. Changes in ownership trigger a reassessment. When there is a change in ownership, the taxable assessed value will be reset to the true assessed value for the subsequent tax year.

Do the cap limitations provided for in Act 2024-344 sunset?

The limitations will continue through the fiscal year beginning October 1, 2027.

Will property taxes still be due each year between October 1 and December 31?

Property taxes in Alabama will still become due and payable each year on October 1 and are considered delinquent if paid after December 31.

I met with the Board of Equalization on my residence. The BOE lowered the market value, but my taxes still increased. Why did this happen?

If after meeting with the county Board of Equalization a taxpayer’s market value is lowered but their tax bill does not reflect the lower market value this could be due to a “gap” between the true assessed value and the taxable assessed value. Until the true assessed value (aligned with market value) and the taxable assessed value are equal, there will be a “gap” between the two values.

I disagree with the market value the county has on my property. Can I still appeal the market value to the county Board of Equalization?

Yes, Board of Equalization Hearings shall continue to function as disputes of a property’s fair market value. Because the cap legislation only affects a property’s assessed value, the role of the County Board of Equalization will not change.

I met with the county Board of Equalization because I disagree with the market value on my property. I do not agree with the decision the board made. Can I appeal to Circuit Court?

Yes, Circuit Court appeals shall continue to function as disputes of a property’s fair market value. Because the cap legislation only affects a property’s assessed value, the role of the Circuit Court will not change.

I added a detached garage and pool on my property; will it be subject to the cap?

Any new improvement (regardless of size or scope) built will exclude the entire parcel from the cap.

My property is included in a new Tax Increment District (TIF). Will my property still be subject to the cap?

Once the new district is created, all parcels in it will then meet the criteria to be excluded from the cap.

My property was in a Tax Increment District (TIF) that was dissolved. Will it now be subject to the cap?

In this case, the affected parcels would no longer meet the criteria for the TIF exclusion. The property would be subject to the cap (unless the parcel meets one of more of the other criteria which would exclude it).

My house had damage due to a natural disaster. Will it still be subject to the cap?

- If repairs are made to remediate damage and return an existing structure to its previous state, the parcel would remain subject to the cap.

- If the existing structure was entirely replaced, or repair work restores the structure to a level beyond its previous state (beyond regular remediation), the property would be excluded from the cap.

I enclosed the attached garage on my house. Will it still be subject to the cap?

If the scope of the work involved in updating an appendage meets the definition of “significant improvement”, the parcel would meet the criteria to be excluded from the cap. The appraisal would be corrected to reflect the change, and the parcel would not be subject to the cap.

I bought a new residence and will now be renting out my previous residence. Will it still be subject to the cap each year?

The parcel will be changing from Class III to Class II, so the entire parcel would be excluded from the cap.

My land is currently under current use, but I am no longer using it for agricultural purposes. Will it still be subject to the cap each year?

If the change in use resulted in a change in assessment class, then the parcel would be excluded from the cap for the current tax year. However, if the assessment class did not change, the parcel would remain subject to the cap (unless the parcel meets one or more of the other criteria which would exclude it).

My husband and I jointly owned property, and he passed away. The property is now solely in my name. Will the property no longer be subject to the cap?

The property would remain subject to the cap since the husband’s ownership in the property was transferred to his spouse upon his death. Per the law, this type of change in ownership would not cause the property to be excluded from the cap.

I purchased a business and decided to keep the LLC name the same. Will the property still be subject to the cap?

In this scenario the parcel would remain subject to the cap. LLCs are considered legally separate entities from their owners, for assessment purposes, ownership of the property never changes because it stays in the same legal entity’s name.

I was deeded my mother’s parcel while she retained a life estate. My mother has now passed away. Will the property be subject to the cap or will it be excluded since my mother has passed away?

In this scenario, the cap would remain for the tax because ownership was assumed by a family member. However, if ownership was assumed by a non-family member, then the parcel would be excluded from the cap for the tax year. NOTE: The parcel could still meet other criteria that would exclude it from the cap.

Definitions of Key Terms

- Cap – A limit on the percentage increase in taxable assessed value of a parcel of Class II real or Class III real property from one year to the next, not to exceed seven percent. The cap only applies to increases in assessed values and does not set a limit on decreases in assessed values. The cap does not impact the calculation of state or local fees (fire, timber, garbage, etc.) or other similar assessments that are determined independently of a parcel’s assessed value. The cap does not apply to the calculation of the assessed value of business personal property.

- Family Member – Includes a child, sibling, parent, grandparent, or grandchild. It also includes stepparents, stepchildren, stepsiblings, and adoptive relationships. This term also includes a spouse unless the law makes a separate, specific reference to that individual.

- Ordinary Maintenance – Routine updates and maintenance to existing structures, including the refurbishment or replacement of components to meet current market expectations. This term would include activities such as painting, changing flooring, repairing or replacing roofs, replacing fixtures, replacing or upgrading existing HVAC, electrical, plumbing, or other similar systems, etc. This term would exclude significant improvements to an existing structure.

- Significant Improvement – An enhancement to a property that exhibits fundamental changes, encompassing multiple alterations that increases its market value and was not included in its appraised value for the preceding tax year. Significant improvements can include, but are not limited to:

- Structural Additions: Adding new rooms, garages, or other major expansions to an existing improvement in which significant finish or structural modifications have been made that enhance utility and attractiveness, involving complete replacement or expansion.

- Extensive Remodeling or Renovation: Major updates to existing rooms, such as kitchens or bathrooms, or comprehensive renovations of entire floors or sections of the property. Alterations may include replacing major components, relocating plumbing fixtures and appliances, and making structural alterations (e.g., moving walls or adding square footage). This includes any structures that have undergone a complete gut rehab.

- Installation of New Systems: Installation of HVAC systems, electrical systems, plumbing systems, or any other major infrastructure.

- Repair of Damaged/Destroyed Improvements: Making significant structural repairs to an existing improvement which was damaged or destroyed, regardless of whether the damage or destruction was done intentionally or was the result of natural disaster or manmade causes. However, repairs to remediate damage that return the improvement to its previous state shall not be considered a significant improvement.

- Other Improvements: Any other enhancements that substantially alter the structure or functionality of the parcel, such as constructing outbuildings, pools, or other similar projects.

- Tax Increment District – A contiguous geographic area within the boundaries of a public entity defined and created by a resolution of a local government body pursuant to Chapter 99 of Title 11, Code of Ala. 1975.

- Taxable Assessed Value – the assessed value of a parcel (before the application of any exemptions) which will be used to compute taxes for a given year. This will either be the property’s true assessed value or its assessed value after the application of the cap, whichever is lower. This value would include the application of any errors, supplements, credits, etc.

- True Assessed Value – The assessed value of a parcel which is determined by multiplying fair market value or current use value by the appropriate assessment rate for the class of property pursuant to §40-8-1, Code of Ala. 1975. This value would include the application of any errors, supplements, credits, etc. This value would also include an assessed value computed from the market value set by a county’s Board of Equalization.

- Property Assessment Classifications:

| Class | Description | Assessment Percent |

| I | All property of utilities used in the business of such utilities | 30% |

| II | All property not otherwise classified | 20% |

| III | All agricultural, forest, and single-family owner-occupied residential property, including owner occupied residential manufactured homes located on land owned by the manufactured home owner, and historic building and sites | 10% |

| IV | All private passenger automobiles and motor trucks of the type commonly known as “pickups” or “pickup trucks” owned and operated by an individual for personal or private use and not for hire, rent, or compensation | 15% |

Additional Information

Further information can be found in §40-7-2.2, Code of Ala. 1975

Your Role in the Process

No Application Needed – The new assessed value cap applies automatically to eligible Class II real and Class III real properties. You do not need to take any action to benefit from the cap. Each year, your local assessing office will determine whether your property qualifies and calculate the taxable assessed value accordingly.

As a property owner, staying informed about your property’s assessed value and how the cap applies to your situation is essential. Regularly review your annual property tax notices and report any changes, such as significant improvements, to your local assessing office.

This page will be updated as new guidance and FAQs become available. For more information, contact your local county assessing office or the Property Tax Division.