For projects granted a sales and use tax abatement, the state sales tax (excluding the 0.75% unabated portion) and the local sales and use taxes not earmarked for education are abated on qualifying tangible personal property incorporated into the project.

To utilize the abatement, all qualifying purchases must be made using a Sales and Use Tax Exemption Certificate for an Industrial or Research Enterprise Project. The certificate is issued to the private user (and, if applicable, its general contractor and subcontractors) and allows qualifying purchases to be made without payment of sales and use tax to the vendor.

The certificate holder is not required to file or remit state use tax on qualifying purchases. However, if the exemption certificate is used for items that do not qualify for the abatement, the applicable state and local taxes must be reported and paid.

The certificate holder is also required to:

- File and remit the Unabated State Sales Tax Return for the 0.75% state tax; and

- Remit any local sales and use taxes earmarked for education, either through ALDOR or directly with the local taxing authority, as applicable.

The certificate of exemption is effective as of the date the abatement is granted and expires upon completion of the project.

To receive a Sales and Use Tax Exemption Certificate for an Industrial or Research Enterprise Project, a contractor must apply for the sales and use tax exemption certificate by providing the necessary documents to the Office of Economic Development as provided below.

General Contractor Application

If you are a general or a prime contractor working on an approved abatement project, and will be making purchases of tangible personal property on behalf of a company that has been granted an abatement, then you must submit the following documents to the Office of Economic Development:

- Form ST: EX-A2 – Application for Sales and Use Tax Certificate of Exemption.

- A letter from the private user on their company letterhead, stating that the general or prime contractor will be making purchases of tangible personal property to be incorporated into the abated project.

- A list of subcontractors (if applicable). The list shall be provided on the general or prime contractor’s letterhead. The list may be updated as needed.

Sub-contractor Application

If you are a sub-contractor working on an approved abatement project and will be making purchases of tangible personal property on behalf of a company that has been granted an abatement, then you must submit the following documents to the Office of Economic Development:

- Form ST: EX-A2 – Application for Sales and Use Tax Certificate of Exemption.

- A signed letter from the private user or the general contractor approving the sub-contractor that will be making purchases of tangible personal property to be incorporated into the abated project. The letter must be submitted on the appropriate company letterhead.

Extension Request

A contractor or a subcontractor can only request the extension once the private user has been approved an extension through our office.

Important Notes about the Sales and Use Tax Certificate of Exemption

- Certificates are not transferable and may only be used by the person, firm, or corporation whose name appears at the bottom of the certificate.

- The certificate is not authorized to be used for purchases which do not qualify for the abatement.

- Contractors are considered the end user and are responsible for remitting the applicable sales or use tax on their purchases of building material, equipment, etc., for construction projects. However, the sales and use tax certificate of exemption will allow the contractors to make direct purchases without paying tax to the seller, but they will be responsible for remitting the unabated state taxes using the Unabated State Sales Tax Return, and the unabated local tax directly to ALDOR or the proper local tax administrator, even if they hire a subcontractor to provide the installation aspect of the contract. See Contractors Liability Rule 810-6-1-.46(5) for further details. The same tax responsibility applies to subcontractors that are hired to perform work on the project and will also make direct purchases of building material that they are responsible for installing/incorporating into the project.

Frequently Asked Questions

- Can a general contractor make copies of the Sales and Use Tax Exemption Certificates and distribute to their subcontractors to make purchases on behalf of a project? Each contractor or a subcontractor must apply for their own certificates of exemption. Certificates are not transferable and may only be used by the person, firm, or corporation whose name appears at the bottom of the certificate.

- Can the applications or extension requests for Sales and Use Tax Certificates of Exemption be made online? These requests can be mailed or emailed to incentives@revenue.alabama.gov.

- Would the contractors/sub-contractors purchase of ‘tools’ for the specific construction project, such as drill bits, saw blades, welding equipment, hard hats, safety glasses, gloves for workers, battery packs for tools, caulking guns, painting rollers, brushes, tape, rags, etc., qualify for sales tax abatement? Miscellaneous tools and supplies that are purchased by the contractor would not qualify for the abatement exemption. However, miscellaneous tools and supplies purchased by the private user that will remain at the project site, will be owned by the private user for federal income tax purposes, and added to the capital account would qualify for the abatement exemption.

- Do costs for travel, such as the sales tax paid for the contractor’s hotel, meals and travel, all related to the construction project, qualify for sales and use tax abatement? These costs do not qualify for the abatement exemption. The abatement exemption applies to the purchase of tangible personal property that will be incorporated into the qualifying project.

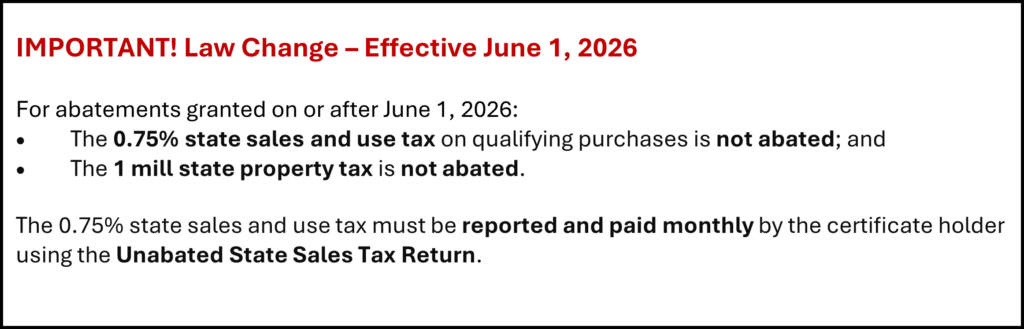

- What is the unabated state sales tax ?

- For abatements granted on or after June 1, 2026:

- The 0.75% state sales and use tax on qualifying abatement purchases is no longer eligible for abatement and must be reported and paid monthly by the certificate holder using the Unabated State Sales Tax Return.

- I am not an owner of an abatement project. Do I still need to file the Unabated State Sales Tax Return? Yes. Effective for abatements granted on or after June 1, 2026, any subcontractor or general contractor that holds the certificate of exemption and makes qualifying purchases for an abated project is required to file the Unabated State Sales Tax Return and pay the unabated 0.75% state sales tax.

- What is unabated local tax, and how do I determine the rates? The unabated local tax is a special rate that some localities have earmarked specifically for education, and these rates cannot be abated/exempt. The abatement statute requires the certificate holder/purchaser to self-remit this tax. To determine the proper local tax rate, please go to Tax Rates, select the appropriate city and/or county and view details.

- Where can I find a list of the unabated locality codes and contact information? Please click here for details.

- I am a sub-contractor that has hired another sub-contractor to perform work on an abatement project. Do I have to provide the confirmation letter to my sub-contractor? Yes, the sub-contractor was hired directly by your company to perform work on the abated project, so you are giving them authorization/approval to make purchases.

- I have been working on a project that was granted an abatement and did not know that I could apply for a certificate of exemption. Is it too late to apply? If the purchases that were made qualify for the abatement, and they were made during the effective/expiration dates specified on the certificate, you can still apply. You can also request a refund of the taxes and self-remit the unabated local tax to ALDOR or the appropriate local tax administrator.